The Battle Between Camera Brands is Once Again Focused on Lenses

The mark of a mature camera system is the breadth and depth of lenses that are available for it. The most recent news swirling around Canon, its RF mount, and third-party lens manufacturers demonstrates the principal battleground between competing mirrorless brands.

Camera sales are so much more than just cameras. One of the reasons for the success of the original Nikon F system was the immediate availability of a wide range of lenses which was fleshed out into one of the broadest systems around. This points to a key selling point for consumers: they want to see a wide range of accessories, and specifically lenses, available. This not only means that they can get the lens they want — be it a 50mm f/1.8 or a 58mm f/0.95 — but points to the potential success and longevity of a system, meaning their investment in a camera and its accompanying lenses is not short-lived.

However, if you turn this thinking on its head, it points to a key imperative for manufacturers. Lenses lock a photographer into a particular camera system, meaning that not only do you get repeat business, but profit margins can be high on what are increasingly big ticket items.

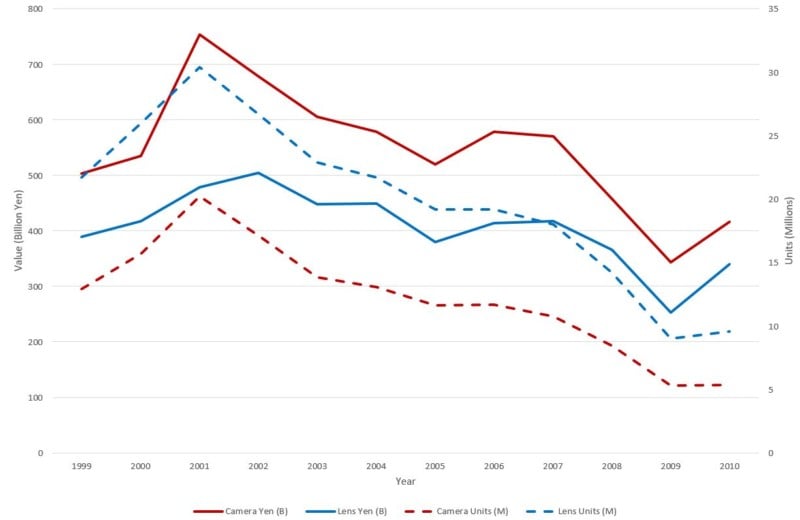

We can clearly see this market structure when we look at CIPA shipment data (see chart below) for interchangeable lens cameras (ILC) and lenses. What this shows is that ILC shipments peaked in 2012 by units and value. And while the total number of ILCs shipped has continued to drop, their value has been far more stable as per unit cost has risen, a result of fewer low-priced items and a choice to target the upper end of the market. On top of this, it’s interesting to note that the relative value of lenses to ILC shipments has remained remarkably consistent, hovering around 43%.

This last point highlights a key aspect of the market today. First-party lenses can be — and are — expensive, making them an important source of income and profit for manufacturers.

In fact, Nikon wants a camera-lens sales ratio of 1:2 (the “lens attach rate”) simply because lenses earn almost as much as cameras. Its target of a lens range of 50 will take time to achieve as the turnover of lens designs is much slower than that of cameras meaning that R&D invested now will have a much longer term (and potentially better) return than cameras. To get an idea, just look at how much your D800 is worth compared to a similar era 70-200mm f/2.8.

What the chart above is slightly misleading about is the volume of the lens market — it’s actually bigger. While camera shipments are broadly accurate, what this means is that the ratio of lens to camera sales is higher. Unlike camera manufacturers who are almost exclusively Japanese, those reporting lens shipments include Canon, Nikon, Sony, Olympus, Tokina, Tamron, Sigma, Panasonic, Cosina, Fuji, Ricoh, and Zeiss. Manufacturers from China and South Korea are excluded, which include Viltrox and Samyang, with suggestions that they may make up about 20% of sales currently.

It’s About the System

To misquote Bill Clinton, it’s about the system. The system attracts consumers by dint of lens availability and long-term support. Giving your system breadth is important as it attracts those camera sales and follow-on lens sales. It also ties your customer into a long-term relationship with you. However, filling out a lens system is time-consuming and expensive, something that is painfully apparent watching Nikon and Canon expand their offerings since they entered the full-frame mirrorless market in 2018.

There are three approaches to fleshing out a camera system, all of which we are seeing at the moment. The first has been adopted by both Fujifilm and Sony who tested the mirrorless waters and have slowly built out a range of amateur and professional lenses to offer an enviable breadth that covers a wide range of bases. This has generated a loyal following of photographers with repeat lens sales. The success of these systems has also encouraged third-party manufacturers.

The second option — a variant on the above — is to rapidly build out a range; this is something that Canon, in particular, has been trying to achieve. This is a riskier and more expensive option as you need to invest the research and development up-front before the success of the system is guaranteed or significant income is generated. In Canon’s case, this isn’t really a problem as it has been able to transfer its DSLR market dominance into the mirrorless realm.

The third option is to form a consortium of manufacturers around a lens mount to produce both cameras and lenses that are all mutually supportive and — broadly — don’t compete with one another. We have seen Leica attempt this with the L-Mount Alliance originally comprising Leica, Sigma, and Panasonic — DJI has since joined. All of them have produced full-frame cameras — of vastly differing styles — that sit alongside Leica’s and Sigma’s complimentary lens ranges. This has the significant benefit of rapidly filling out the camera and lens offerings, as long as any single member doesn’t want to monopolize the system. On face value, the L-Mount Alliance seems to have found a good balance.

The final option is to bring third-party manufacturers on board relatively early to expand the lens offerings in order to rapidly fill out and accessorize a system at the expense of ownership.

In some sense, we have seen this with Fujifilm and Sony. While PetaPixel has confirmed that Fujifilm has licensed its mount, Sony did several years ago which has resulted in a glut of first and third party optics options. Given that the X-mount and E-mount both have APS-C variants, third-party manufacturers have achieved market scale, at minimal cost, in a way an own brand wouldn’t be able to achieve. Full-frame lenses had more limited appeal when only Sony was in the mirrorless market, but with the newer Nikon Z-mount and Canon RF-mount, the time is ripe to offer a range of lenses.

Latest Developments

Some recent developments in the lens market have highlighted the differences we are seeing above. Firstly, there has been a switch from low-cost brands moving from manual to auto-focus lenses. This requires a much greater degree of development, but the scope of the market clearly makes this worthwhile.

Secondly, we are now seeing top-end third-party manufacturers — particularly Sigma and Tamron — expanding their mirrorless mount offerings. This is most notable with the recent announcement by Tamron of the first third-party zoom lens available for the Z-mount which we were able to verify is licensed from Nikon. This is important for Nikon, at a time when its market share is low, as it increases the visibility and viability of the system, while for Tamron it potentially expands an exclusive offering. It is also similar to the approach Nikon has taken with its strobe system.

Thirdly, Canon recently confirmed it ordered Viltrox to cease producing autofocus RF lenses on the basis of patent infringement. It’s possible that reverse engineering of the lens communication — as opposed to the physical mount — has fallen foul of Canon’s intellectual property. Either way, it suggests that Canon will use its market dominance to protect both the RF system and the sales it represents. Whatever the case, it’s a bad look.

It’s also possible that we are seeing the seeds of Nikon adopting the opposite strategy and trying to broaden the diversity and appeal of the Z-mount. If — as PetaPixel has reported — Nikon is repositioning its Imaging Division to take a backseat in the business, then this may well be a pragmatic approach to maintain the long-term survival of camera manufacturing.

The Future

Consumers are, in general, spoiled by the lens offerings from own-brand manufacturers, however, there has long been demand and a market for third-party manufacturers. This is particularly the case for common focal lengths, of good quality, at competitive prices. With the ongoing development of mirrorless systems, we are seeing the rebirth of new lens ranges within a highly competitive environment.

Only time will tell which approach is ultimately the most successful, but ask yourself this question: if you weren’t not allowed by purchase third party lenses, would you buy-in to that camera system?

Image creditsHeader photo licensed via Depositphotos.

Affiliate Disclosure PetaPixel articles may include affiliate links; we may earn a commission if you buy through one.