Why Kodak Died and Fujifilm Thrived: A Tale of Two Film Companies

The Kodak moment is gone, but today Fujifilm thrives after a massive reorganization. Here is a detailed analysis based on firsthand accounts from top executives and factual financial data to understand how and why the destinies of two similar companies went in opposite directions.

The Situation before the Film Crisis: A Profitable and Secure Market

Even though Kodak and Fujifilm produced cameras, their core business was centered on film and post-processing sales. According to Forbes, Kodak “gladly gave away cameras in exchange for getting people hooked on paying to have their photos developed — yielding Kodak a nice annuity in the form of 80% of the market for the chemicals and paper used to develop and print those photos.”

Inside Kodak, this was known as the “silver halide” strategy named after the chemical compounds in its film. It was a fantastic success story. This business strategy was similar to Gillette’s or that of printer manufacturers: give away razors or printers to make money on blades and ink cartridges. Indeed, Fujifilm introduced the disposable 35mm camera to the masses in 1986 before being joined by Kodak in 1988. Film was everything to them.

In 2000, just before the digital transition, sales related to film accounted for 72% of Kodak revenue and 66% of its operating income against 60% and 66% for Fujifilm.

Photo film is made of a fine-tuned combination of various technologies and requires a careful manufacturing process. A quick look at the cross-section of a color film reveals that on a clear base film (TAC), there are 20 evenly coated layers, each sensitive to the three primary colors of light, red, blue, and green. Each of these overlapping layers is only one micron thick.

The CEO of Fujifilm, Mr. Shigetaka Komori explains in his book that “in addition to film formation and high-precision coating, there are grain formation, function polymer, nano-dispersion, functional molecules, and redox control (oxidation of the molecule). Inherent in all these is very precise quality control.”

Willy Shih, former vice president of Kodak (1997-2003) also confirms that “Color film was an extremely complex product to manufacture.” The film roll “had to be coated with as many as 24 layers of sophisticated chemicals: photosensitizers, dyes, couplers, and other materials deposited at precise thicknesses while traveling at 300 feet per minute. Wide rolls had to be changed over and spliced continuously in real-time; the coated film had to be cut to size and packaged, all in the dark.”

Mr. Komori remembers that back in the day, there were at one time 30 or 40 producers of monochrome photo film in existence globally but many of these companies were confronted by an insurmountable technical wall with the advent of color film. “With film, the entry barriers were high. Only two competitors, Fujifilm and Agfa-Gevaert, had enough expertise and production scale to challenge Kodak seriously,” Shih said.

The film business was relatively secure and profitable. The market was animated for decades by the Fuji-Kodak duel, while Agfa and Konica played in the second and third leagues. Each company had prominent shares in their domestic market which generated a continuous and safe stream of revenue despite temporary price wars like the one launched by Fuji against Kodak in the 80s and 90s.

The Consequences of the Digital Revolution: A “Crappy” and Vanishing Business

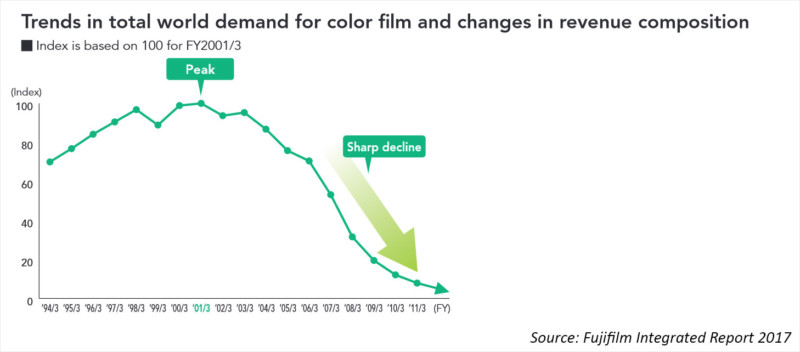

In 2001, the film sales peaked worldwide but as the president of Fujifilm remembers: “a peak always conceals a treacherous valley.” First, the market began shrinking very slowly, then picked up speed and finally plunged at the rate of twenty or thirty percent a year. In 2010, worldwide demand for photographic film had fallen to less than a tenth of what it had been only ten years before.

But, initially, the market didn’t vanish, it changed. Following the internet and personal computer democratization of the 90s, consumers started to purchase digital cameras. Unfortunately, for film manufacturers, the transition from analog to digital imaging represented tremendous difficulties. First, the semiconductor technology platform had nothing to do with film manufacturing.

But most importantly, as the former vice president of Kodak explains: “The broad applicability of the technology platform meant that a good engineer could buy all the building blocks and put together a camera. These building blocks abstracted almost all the technology required, so you no longer needed a lot of experience and specialized skills. Suppliers selling components offered the technology to anyone who would pay, and there were few entry barriers.”

In other words, the digital era was the exact opposite of the comfortable “silver halide” business model where a few players shared a secured market with good margins. The core business of film and post-processing disappeared, but the commercialization of digital cameras didn’t make up for the loss. In 2006, the CEO of Kodak, Antonio Perez was quoted calling digital cameras a “crappy business.”

Why? Because all of a sudden, Kodak and Fujifilm were forced to leave their quasi-duopoly and compete against dozens of companies in the low-margin business of digital cameras. Unlike color films, anyone could put a sensor and processor together and introduce a product to the market. And that’s precisely what happened. As Yukio Shohtoku, retired executive vice president of Panasonic said to his Kodak counterpart, “Modularization makes consumer products, our consumer products, a commodity.”

This explains how a California surfer could appear out of nowhere and take the consumer video recorder market by storm as the CEO of GoPro did before being overrun, in turn, by cheaper Chinese electronics manufacturers.

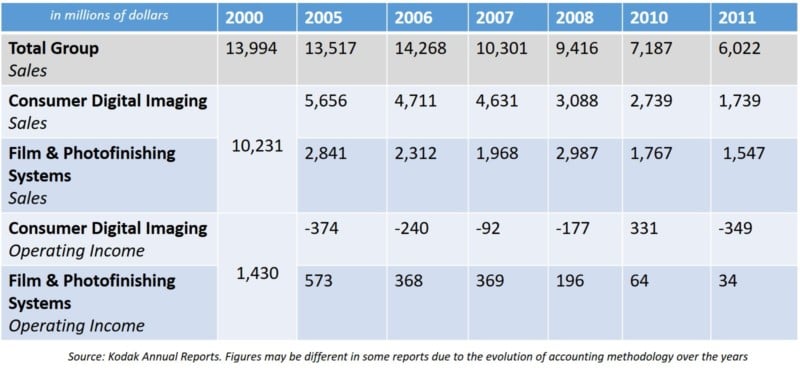

A quick look at Kodak’s finance shows this situation. In the early 2000s, Kodak managed to maintain its level of sales, but the profits of the group plunged into the negative zone. In the ’90s, Kodak Sales were oscillating between 13 and 15 billion with average net earnings of 5-10%. The company generated $1.4 billion in profit in 2000 and $800 million in 2002. After that, the finance of the Rochester-based corporation suffers a long agony leading to a bankruptcy filing in 2012. The drop is especially sharp after 2006.

The issue was not about selling cameras, Kodak sold plenty of digital cameras. In 2005, Kodak captured 21.3% of the US market share and emerged first in the digital camera segment against its Japanese rivals. That year, the US group managed to grow its sales by 15%.

Unfortunately, the sales were not as good worldwide. Kodak reached an early lead in the market and had a 27% market share by 1999. But that slipped to 15% by 2003 and 7% by 2010, as Kodak ceded ground to Canon, Nikon and others.

The main problem was that Kodak was not making money with digital cameras. It was bleeding cash. According to a Harvard case study, it lost $60 for every digital camera it sold by 2001.

This issue appears clearly in the financial reports. Whereas in 2000 Kodak made an operating income of $1.4 billion out of $10.2 billion in sales in the photography division, the profitability quickly vanished afterward.

In 2006, the official annual report started to separate the sales figure from the digital and film segment. As we can see in the chart below, Kodak initially maintained a somehow decent level of revenue from the photography division. It even managed to replace declining film sales with digital imaging revenue, but this activity was making losses. Eventually, Kodak had to file for bankruptcy in 2012. The previous year, film sales only generated an operating income of $34 million while the digital camera division lost ten times that ($349 million loss).

The big picture was not better for Fujifilm as it faced the same storm as its American competitor. The president of Fujifilm remembers that “what we could not account for in our projections was the speed of the digital onslaught. The photographic film market had shrunk much faster than we expected.” Between 2005 and 2010, the sales of color film declined from 156 billion yen to 33 billion while the photo finishing segment shrunk from ¥89 billion to ¥33 billion. Not only did the Japanese company overcome the crisis, but it thrived in this challenging environment. How?

How Did Fuji Overcome the Crisis and Thrive?

The critical element in Fujifilm’s success is diversification. In 2010, the film market dropped to less than 10% compared to 2000. But Fujifilm, which once made 60% of its sales with film, diversified successfully and managed to grow its revenue by 57% over this ten years period while Kodak sales fell by 48%.

Faced with a sharp decline in sales from its cash cow product Fujifilm acted swiftly and changed its business through innovation and external growth. Under the decisive grip of Shigetaka Komori, appointed president in 2000, Fujifilm quickly carried out massive reforms. In 2004, Komori came up with a six-year plan called VISION 75 in reference to the 75th anniversary of the group. The goal was simple and consisted of “saving Fujifilm from disaster and ensuring its viability as a leading company with sales of 2 or 3 trillion yen a year.”

First, the management restructured its film business by downscaling the production lines and closing redundant facilities. In the meantime, the research and development departments moved to a newly built facility to unify the research efforts and promote better communication and innovation culture among engineers. But realizing that the digital camera business would not replace the silver halide strategy due to the low profitability of his sector, Fujifilm performed a massive diversification based on capabilities and innovation.

Even before launching the VISION 75 plan, the president ordered the head of R&D to take inventory of Fujifilm technologies and compared them with the demand of the international market. After a year and a half of technological auditing, the R&D team came up with a chart listing the all existing in-house technologies that could match future markets.

The president saw that “Fujifilm technologies could be adapted for emerging markets such as pharmaceuticals, cosmetics, and highly functional materials.” For instance, the company was able to predict the boom of LCD screens and invested heavily in this market. Leveraging the photo film technologies, the engineer created FUJITAC, a variety of high-performance films essential for making LCD panels for TV, computers, and smartphones. Today, FUJITAC owns 70% of the market for protective LCD polarizer films.

The company also targeted unexpected markets like cosmetics. The rationale behind cosmetics comes from 70 years of experience in gelatin, the chief ingredient of photo film which is derived from collagen. Human skin is seventy percent collagen, to which it owes its sheen and elasticity. Fujifilm also possessed deep know-how in oxidation, a process connected both to the aging of human skin and to the fading of photos over time. Thus, Fujifilm launched a makeup line in 2007 called Astalift.

When promising technologies that could match growing markets didn’t exist internally, Fujifilm proceeded by merger and acquisition (M&A). To develop new business ventures, the group made active use of M&A. By acquiring companies that already penetrated a market and combine their assets with Fujifilm’s expertise, the Japanese firm could release new products to the market quickly and easily.

Based on technological synergies, it acquired Toyoma Chemical in 2008 to enter the drug business. Delving further into the healthcare segment, Fujifilm also brought a radiopharmaceutical company now called Fujifilm RI Pharma. It also reinforced its position in existing joint ventures such as Fuji-Xerox which became a consolidated subsidiary in 2001 after Fujifilm purchased an additional 25% share in this partnership.

In 2010, nine years after the peak of film sales, Fujifilm was a new company. Whereas in 2000, 60% of its sales and two-thirds of the profit came from the film ecosystem, in 2010 the Imaging division accounted for less than 16% of the revenue. Fujifilm managed to ride out of the storm via a massive restructuring and diversification strategy.

Why Did Kodak Fail?

A lot has been said about Kodak’s failure to reform itself. The usual story describes a mummified company stuck in the analog era and incapable of adapting to the digital world. Some explained that Kodak suffered from Myopia and didn’t see the digital camera coming while other said that complacency was the cause of the problem since the senior management refused to accept the inevitable even though they were aware of the incoming digital Tsunami.

While this narrative carries a certain truth, it is simplified and incomplete. As mentioned previously, Kodak did build a decent range of digital cameras and managed to rank first in US sales for a while in the early 2000s. Historically, Kodak was the inventor of the digital camera when it developed this technology back in 1975. The Rochester company poured billions of dollars into the digital R&D, and like Fujifilm, performed a massive downscaling effort that also cost billions.

According to the Harvard Business Review: “CEO George Fisher (1993-1999) knew that digital photography might eventually invade, or even replace, Kodak’s core business. Doubtless, he and other senior executives were tempted to ignore it. To their credit, they resisted that temptation. Fisher rallied the troops and aggressively invested more than $2 billion in R&D for digital imaging.” An effort pursued by the next CEO Dan Carp who vowed to invest two-thirds of the company’s research and development budget on digital projects.

The former president of Kodak’s consumer digital business adds that “Kodak management has been criticized for compromising its digital efforts because it wanted to protect film. But the criticism is overblown. Responding to recommendations from management experts, from the mid-1990s to 2003 the company set up a separate division (which I ran) charged with tackling the digital opportunity. Not constrained by any legacy assets or practices, the new division was able to build a leading market share position in digital cameras.”

In reality, Kodak failed for the same reason that Fujifilm succeeded: diversification. But for Kodak, it was the lack of diversification that condemned this firm to fade. Unlike Fujifilm which recognized early on that photography was a doomed business and tackled new markets with a completely different portfolio, Kodak made a wrong analysis and persisted in the decaying photo industry.

Essentially, it’s not that Kodak didn’t want to change, it tried hard, but it did it wrong. Faced with a radical market disruption, it reacted energetically, but doing something and doing the right thing is different. As Kodak’s former Vice President explains, “Kodak management didn’t fully recognize that the rise of digital imaging would have dire consequences for the future of photo printing.” In the late 90s, Kodak hastily installed 10,000 digital kiosks in Kodak’s partner stores. Simply put, Kodak tried to replicate the silver halide business model in the digital world. At least, the printing part of it.

Unfortunately, “the business they built failed in the traditional market and also failed to find a new market. Industry outsiders—Hewlett-Packard, Canon, and Sony—did a better job. They launched products based on home storage and home printing capabilities and, in the process, uncovered new demand for convenience, storage, and selectivity” explained the Harvard Business Review in 2002. Two years later, Facebook was born, and soon after that, prints became a thing of the past. The majority of consumers were not going to print pictures anymore. Instead, they shared them online.

Kodak understood the stake of digitalization, invested in the technology, and foresaw that pictures would be shared online. For instance, they acquired a photo-sharing website called Ofoto in 2001. Unfortunately, the company used Ofoto to make people print digital pictures. They failed in realizing that online photo sharing was the new business, not just a way to expand printing sales.

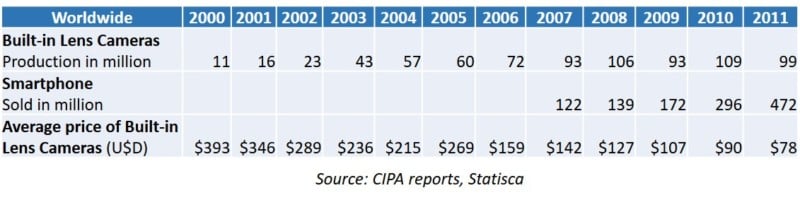

But the decline of prints came with difficulties in the mass market for standalone digital cameras. According to Mr. Shih, head of the Consumer Digital Imaging division at Kodak, the position of his newly created division “was essentially decimated soon thereafter when smartphones with built-in cameras overtook the market.” As soon as 2003, camera phones outsold digital still cameras worldwide, and the smartphone sales grew at a much faster pace than the demand for point and shoot camera. As the CEO of Kodak said in 2006, it was a “crappy business.” The average price of a digital camera in 2000 was $393, but this figure plunged to $78 in 2012.

No matter how hard Kodak tried; photo prints became a minor market while the entry-level camera was a low-profit game dominated by other players. In this environment, the survivors were semiconductor manufacturers, designing and selling technological modules for cameras or smartphones (Sony) or DSLR makers like Canon and Nikon which specialized in the high-end niche of interchangeable lens cameras. Kodak was neither of those as it only sold basic cameras.

To make matters worse, “Kodak withdrew early on from developing and manufacturing its own digital cameras to rely on OEM manufacturers instead. Not having its own technology such as sensor and image processing put Kodak at a considerable disadvantage when the digital race began in earnest” explains the CEO of Fujifilm, Mr. Komori.

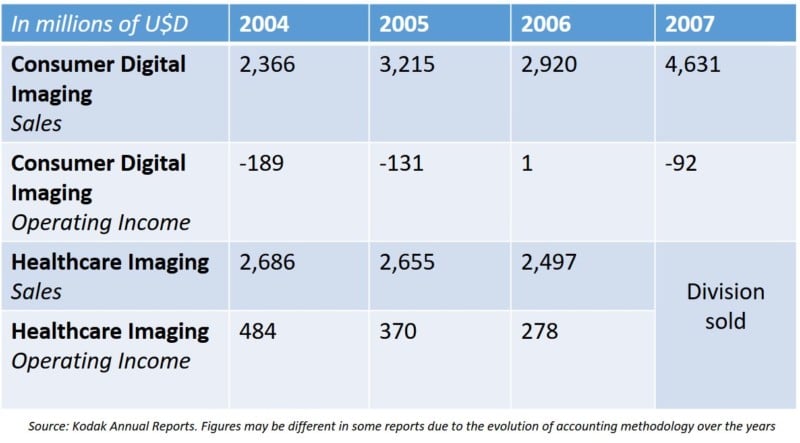

Surprisingly, Kodak persisted in chasing this crappy business. While Fujifilm invested heavily in the pharmaceutical and healthcare sector to reduce its exposure to the challenging photo industry, Kodak sold its highly profitable Healthcare Imaging branch in 2007 to put more resources into its losing consumer camera division. The group pocketed $2.35 billion from the sale, but analysts said it was a bad move to get out of the business when baby boomers were about to retire in droves, and demand for X-rays would increase. For the CEO of Fujifilm, getting rid of this profitable healthcare division was a “fatal mistake.”

Why did Kodak leaders make such a mistake? Why did they persist to capture a vanishing low-margin business when other companies had a technological edge over them?

“In law, we call it, a bird that likes to fly backward. Because it’s more comfortable looking where it’s been than where it’s going,” said Dan Alef, the author of a biography on George Eastman (founder of Kodak).

Retrospectively, Mr. Shih, the former VP of Kodak thinks that the company “could have tried to compete on capabilities rather than on the markets it was in” like Fujifilm did but “this would have meant walking away from a great consumer franchise. That’s not the logic that managers learn at business schools, and it would have been a hard pill for Kodak leaders to swallow.”

The CEO of Fujifilm confirms this statement and lists inertia as the first reason for Kodak’s downfall. “It was the premier company for so long,” he said, adding that “This I believe, made it slow to adapt. From the outside, it appeared that Kodak deep down just really didn’t want to.”

By contrast, Fujifilm, which was always the challenger in the shadow of Kodak, learned to be bold and innovative to close the gap with the historic leader. As a necessity, its corporate culture was more adventurous and prone to risk. For instance, Fujifilm opened factories in the USA in the 80s, and it dared to challenge the Kodak marketing empire in its backyard when it won the rights to sponsor the 1984 Los Angeles Olympics.

Conclusion

Winston Churchill once said that “History is always written by the winners.” Post-crisis analysis is always a comfortable exercise, and plenty of consultants and business teachers love to mention Kodak as a case study for poor management performance. But history is also based on contingencies. Kodak sold its photo-sharing website Ofoto as part of its bankruptcy plan for less than $25 million in April 2012. That same month, Facebook purchased Instagram for $1 billion. In an alternate universe, Ofoto could have become the leading online image-sharing platform.

The opposite is true for Apple. Today, who remembers that this elitist firm was on the verge of bankruptcy not so long ago? In 1997, after 12 years of financial loss, Microsoft and Steve Jobs came to the rescue. Worried to be viewed as a monopoly without competition from Apple, Microsoft invested $150 million in the dying Apple. The now trillion dollars company came that close to disappearing.

But despite all their efforts, Kodak CEOs Fisher, Carp, and Pérez were no Steve Jobs and history wasn’t on their side. In the heat of the action, when the company was losing billions of dollars, Kodak executives did what they could. In his book, the CEO of Fujifilm talks about leadership and says that the number two leader “uses a Bamboo sword, number one uses steel.”

Mr. Komori meant that when executive leaders fight with “steel swords, to lose means to die” because their decisions have strategic consequences for the future of the company. They can’t afford to be wrong. He remembers how he decided to conduct a massive investment in the FUJITAC film business for LCD screens at a time when no one knew for sure if plasma technology, which didn’t require film, was not going to beat the LCD technology. Uncertain about the outcome, he decided to launch four production lines for LCD film when his managers wanted to start with one.

As a top executive, Komori recalled having many “sleepless nights,” but diversification demanded courage and decisive actions. History was on his side, and this bold move, typical of the Fujifilm philosophy paid off. Today FUJITAC controls 70% of this market worldwide.

Some say Kodak made the mistake that George Eastman, its founder, avoided twice before, when he gave up a profitable dry-plate business to move to film and when he invested in color film even though it was demonstrably inferior to black and white film (which Kodak dominated). However, with the advent of the digital era, it was not about making an evolution in the same industry, it was a matter of conducting a revolution: dropping the crappy digital photo industry and using the internal know-how to diversify in other markets.

Unlike Fujifilm, Kodak couldn’t achieve this vital revolution. When the founder of Kodak, George Eastman, committed suicide in 1932 at the age of 77, he left a note saying “My work is done.” But this time, the work wasn’t done at Kodak.